September 7, 2022 — Silk Road Energy Inc. (SLK.V) reports that Silk Road (Record Gold) has acquired an option agreement on gold exploration properties held by a private exploration company and constitutes a non-arms-length transaction pursuant to an option agreement conveyed on September 6, 2022.

The vendor of the option agreement on the gold properties is Record Gold Corp (“Record Gold”), an Ontario-based private exploration company. The transaction is a “related party transaction” as defined under MI 61-101 as Michael C. Judson is CEO, director and shareholder of Silk Road and President, director and shareholder of Record Gold. David Johnson is Corporate Secretary, director and shareholder of Silk Road and Corporate Secretary and shareholder of Record Gold. Dr. Paul Craig is a director and shareholder of Silk Road and a shareholder of Record Gold.

The private company will exchange its option agreement with Pelangio Exploration Inc. (PX.V) in return for 40 million shares of Silk Road at a price of $0.05 per share. Following the transaction Silk Road will have 68,076,104 issued and outstanding shares.

The Grenfell gold property is comprised of 38 mining cells and eight leased claims covering an area of approximately 6.7 square kilometres and is located approximately ten kilometres northwest of Agnico Eagle’s Macassa Mine (2021 production: 210,192 oz gold) in Kirkland Lake Ontario. Grenfell is also located eight kilometres west of Record Gold’s newly acquired Kenogami East (see August 10, 2022 news release)

Following the conveyance of the option agreement to Silk Road, the option agreement with Pelangio will have the following terms:

Record Gold has the right to earn an undivided 80% interest in Grenfell by completing a total of $2,000,000 in work costs or exploration expenditures to be incurred within five years and by making one-time cash payment to Pelangio.

The work costs shall be completed in accordance with the following schedule: $250,000 must spent on the property twenty-four (24) months from the date of the signing of the Agreement; $500,000 on or before the third anniversary; $750,000 on or before the fourth anniversary; and, $500,000 on or before the fifth anniversary. In addition to the work costs associated with the earn-in agreement, Record Gold shall pay to Pelangio a one-time $60,000 payment in twenty-four (24) months.

“This transaction is a result of a collaboration formed with Pelangio Exploration in 2020,” said Michael Judson, Chairman and CEO of Silk Road. “Pelangio is currently a shareholder of Silk Road and will become a substantial shareholder of our company in return for letting us option one of their most promising and undeveloped gold properties: Grenfell”.

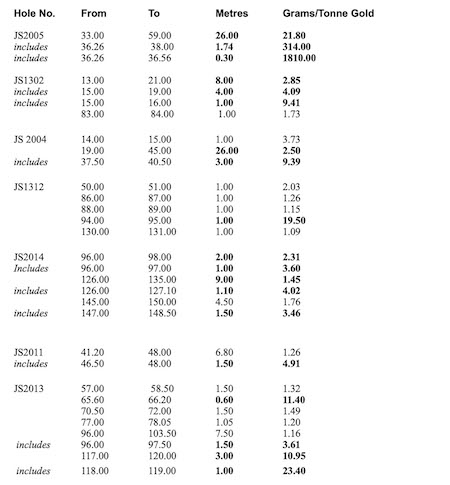

Below is selected assay data from recent drilling on Grenfell:

(Source: * NR Pelangio Exploration Inc March, 2010; ** SGX Asses Rpt J.K.Filo 2013)

The following historical analysis and points of interest are paraphrased from a geological report on the property by John Londry P. Eng. (“Report on the John Sirola Property, Grenfell Township, 1985”). Please note that assay values are not NI 43-101 compliant:

- The majority of work on Grenfell took place in the 1930’s to early 1940’s when bulk sampling of some high-grade gold veins occurred in conjunction with diamond drilling, shaft sinking and substantial lateral development on two underground levels. With renewed interest in the property a series of surface exploration programs were conducted from the early 1980’s to about 2013.

- More recent exploration work and re-evaluation of historical work has resulted in new zones of gold mineralization and recommendations for further exploration on known historical zones from the 1930-1940 era.

- The property hosts five distinct gold-bearing zones. These zones in order of importance are the No.1 Vein, Sirola Vein, No. 6 Vein, Shea Vein and Shaft Vein.

- Significant work was conducted on the No.1 Vein and Sirola Vein. The Sirola Vein is interpreted to be a possible splay vein from the No.1 Vein. Two separate bulk samples from the Sirola Vein (surface pit) and No.1 Vein (60-foot level or 18.3 metres) returned 21.36 tonnes at 0.456 oz/ton gold (15.6 grams/tonne gold) and 174 tonnes at 0.70 oz/ton (24 grams/tonne gold) respectively.

- The No.1 Vein was channel sampled along the drift on the 250-foot (76.3 metres) level which assayed 0.2 oz/ton (6.9 grams/tonne gold) across a 3-foot (.92 metres) width for 180 feet (54.9 metres) of strike. The Londry report also stated that this drift should have continued in an easterly direction on the 250-foot (76.3 metres) level as values and vein structure suggested the vein continued.

- Londry’s report states a third gold bearing zone, the No.6 Vein has a northwesterly trending strike orientation or a transverse strike relative to the No.1 Vein (southwest strike). The No.6 vein was drill tested with only three drill holes, these holes which returned 0.13 oz/ton gold (4.5 grams/tonne gold) over 10 feet (3.05 metres), 2.22 oz/ton gold (76.1 grams/tonne gold) over 3 feet (.92 metres). and 0.25 oz/ton gold (8.6 grams/tonne gold) over 5 feet (1.5 metres).

- The Shea Vein also reported to be northwesterly striking structure is located approximately 700 feet (213.5 metres) southwest of the shaft collar. The 250-level (76.3 metres) drift was extended westward for 700 feet (213.5 metres) to evaluate the Shea Vein mineralization. Very limited data exists on this work but Londry’s report states a single historical drill hole on the Shea Vein returned 0.41 oz/ton gold (19.5 grams/tonne gold) over 3 feet (.92 metres).

- The Shaft Vein was intersected during the course of shaft sinking; the vein entered the shaft at the 90-foot (27.5 metres) level and exited the shaft at the 150-level (45.8 metres). When diluted to a width of one foot (.305 metres), the Shaft Vein returned 0.24 oz/ton (8.2 grams/tonne gold) over the 60-foot (18.3 metres) interval it remained in the shaft.

Completion of the transaction is subject to a number conditions, including TSX Venture Exchange approval, disinterested shareholder approval. There can no assurance that the transaction will be completed as proposed or at all.